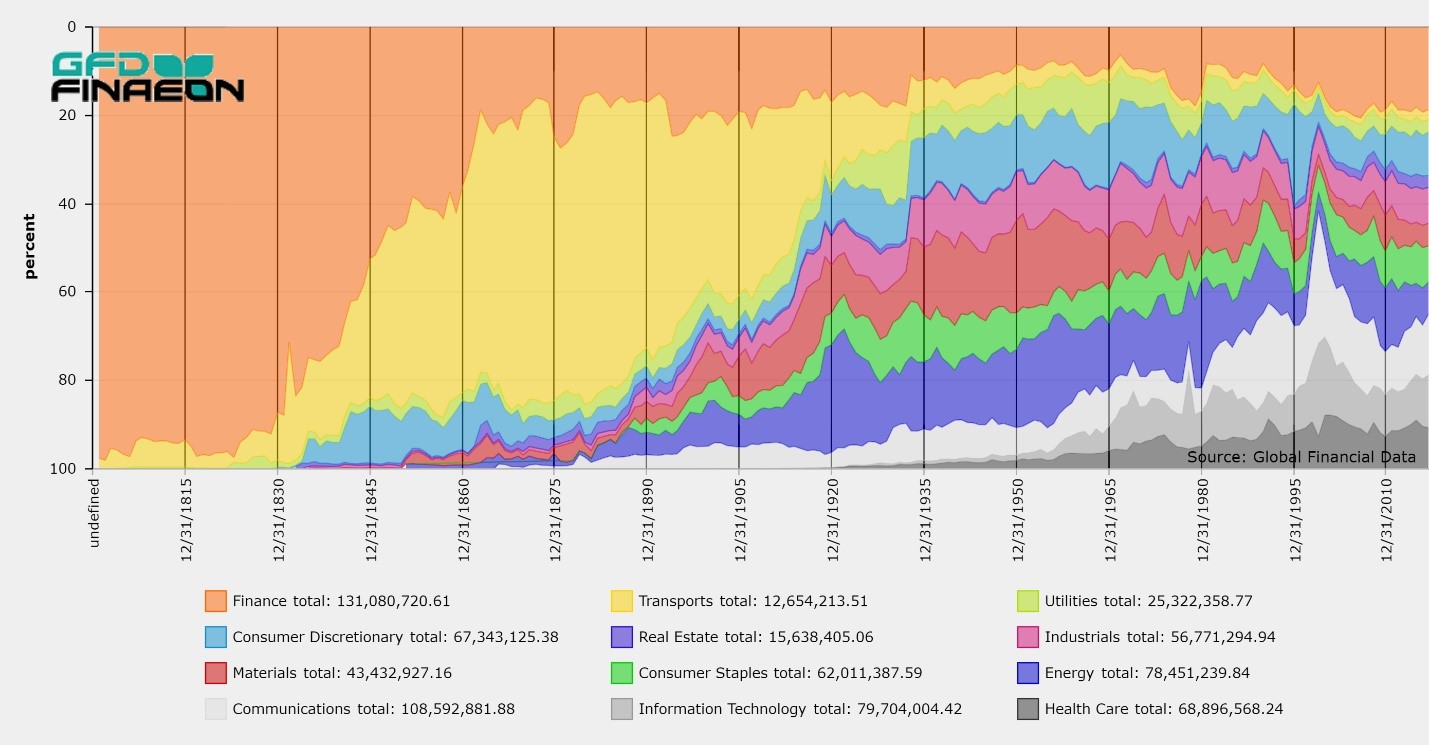

The stock for which Global Financial Data has the longest history is the Bank of England stock, or as it was originally known, the Governor and Company of the Bank of England.

The origin of the Bank of England lies in naval warfare. In 1694, the French had the strongest navy in the world and following the 1690 Battle of Beachy Head, England needed to rebuild its navy, but King William III lacked the resources and the credit to do so.

The stock for which Global Financial Data has the longest history is the Bank of England stock, or as it was originally known, the Governor and Company of the Bank of England.

The origin of the Bank of England lies in naval warfare. In 1694, the French had the strongest navy in the world and following the 1690 Battle of Beachy Head, England needed to rebuild its navy, but King William III lacked the resources and the credit to do so.

This problem was resolved by creating the Bank of England. In exchange for creating a limited liability corporation, which would act as a bank for the government and have the right to issue banknotes, the shareholders would loan the bank £1,200,000 at 8% interest. The Royal Charter was granted on July 27, 1694 and the £1,200,000 was subscribed in only 12 days. Over time, the Bank of England took on the responsibilities of managing the government’s debt, becoming a banker’s bank, controlling interest rates through discounting and establishing a base interest rate, having the exclusive right to issue banknotes within 20 miles of London, and then within the entire country, and the other duties that are now associated with a central bank.

The Bank of England was nationalized on October 29, 1945. Shareholders received £400 in bonds for each £100 in par value of bank stock with bonds paying 3% interest (as opposed to the 12% yield) with bonds redeemable at par on April 5, 1966.

The Bank of England’s stock traded for over 250 years before its nationalization. The stock participated in the South Sea Bubble of 1720, though only doubling in price rather than showing the ten-fold increase South Sea Stock enjoyed before collapsing. The Bank of England stock, along with East Indies Co. stock and South Sea Co. stock were the three companies whose shares were safe enough, because of their government connection, to trade regularly on the London Stock Exchange during the eighteenth century. Until the rise of canals and the liquidity created by the Napoleonic Wars, stock trading remained almost non-existent between 1720 and 1800.

Only British government bonds were safer than Bank of England stock; however, Bank of England stock had the potential for dividend increases that the government stock did not. Although the dividend fluctuated in its first dozen years, the dividend settled down to infrequent changes after the 1720 South Sea Bubble.

Since I grew up in Dallas where the old Dr. Pepper plant was located on Mockingbird Avenue (now demolished), I have always been a Dr. Pepper fan, and though not everyone refers to it as the elixir of life as I do, it is still popular among those with discriminating taste like me, especially if you grew up in Texas.

Since I grew up in Dallas where the old Dr. Pepper plant was located on Mockingbird Avenue (now demolished), I have always been a Dr. Pepper fan, and though not everyone refers to it as the elixir of life as I do, it is still popular among those with discriminating taste like me, especially if you grew up in Texas.

Dr. Pepper has gone through several corporate transitions. The Circle “A” Corp. which had the exclusive right to bottle Dr. Pepper went bankrupt in 1923 and reemerged as Dr. Pepper Co. after incorporating in Dallas in 1923. The Dr. Pepper Co. was acquired by Forstmann and Little, a New York Investment firm, in February 1984. Dr. Pepper merged with Seven-Up in 1986 to form the Dr. Pepper/Seven-Up Companies which went public in 1993 only to be Cadbury Schweppes plc in June 1995. Cadbury Schweppes merged Dr. Pepper/Seven-Up with the Snapple Group to form Dr. Pepper Snapple Group, Inc. in 2007 which went public in May 2008 and still trades on the NYSE.

The first Dr. Pepper shares, which traded on the St. Louis Stock Exchange and OTC before moving to the NYSE on March 18, 1946, had two spectacular moves. The first move occurred between 1934 and 1937 when the stock made a 32-fold move as the company pulled out of the Depression. Since this spectacular move occurred before the stock traded on the NYSE, very few people are aware of this huge recovery in the stock price. The stock traded sideways for the next two decades before making another fabulous rise in the 1960s. Between 1960 and 1972, Dr. Pepper Stock made a 64-fold move. Even though Dr. Pepper wasn’t one of the “Nifty Fifty” stocks from the 1960s, it should have been. Between these two moves in the 1930s and the 1960s, Dr. Pep

per made a 480-fold move, making it one of the best-performing stocks of the twentieth century.

per made a 480-fold move, making it one of the best-performing stocks of the twentieth century.

per made a 480-fold move, making it one of the best-performing stocks of the twentieth century.

Unless you have the complete history of Dr. Pepper to see how it performed prior to joining the NYSE in 1946, you wouldn’t have known that Dr. Pepper had already made one spectacular move, had built a 25-year base, and was ready to join the Hall of Fame of Outstanding stocks. True stock analysts shouldn’t only worry about the survivorship bias that comes from ignoring delisted stocks, but from the exchange bias that comes from ignoring the pre-NYSE history of a stock as Dr. Pepper clearly illustrates.

Even though the Fed is not due to raise interest rates for a few years (2016 per the latest numbers that I’ve seen lately). People are still looking and preparing for this to happen. What asset classes will be affected positively and negatively? In the graph attached, I wanted to show the inverse correlation between preferred stocks and interests rates. with the recent move in rates, the price performance of preferred stocks has been negative. Please look at this long-term graph and see for your self

Even though the Fed is not due to raise interest rates for a few years (2016 per the latest numbers that I’ve seen lately). People are still looking and preparing for this to happen. What asset classes will be affected positively and negatively? In the graph attached, I wanted to show the inverse correlation between preferred stocks and interests rates. with the recent move in rates, the price performance of preferred stocks has been negative. Please look at this long-term graph and see for your self

Freddie Mac has added 23 new Metropolitan Standard Areas (MSAs) to the list of MSAs that they cover in their quarterly surveys of housing prices throughout the United States. The FMHPI provides a measure of typical price inflation for houses within the U.S. Values are calculated monthly but are released at the end of the following quarter. The FMHPI is based on an ever expanding database of loans purchased by either Freddie Mac or Fannie Mae.

With the addition of the 23 new MSAs, the Freddie Mac survey now covers 383 MSAs throughout the United States. The 23 new MSAs are:

Freddie Mac has added 23 new Metropolitan Standard Areas (MSAs) to the list of MSAs that they cover in their quarterly surveys of housing prices throughout the United States. The FMHPI provides a measure of typical price inflation for houses within the U.S. Values are calculated monthly but are released at the end of the following quarter. The FMHPI is based on an ever expanding database of loans purchased by either Freddie Mac or Fannie Mae.

With the addition of the 23 new MSAs, the Freddie Mac survey now covers 383 MSAs throughout the United States. The 23 new MSAs are:

- Albany, OR Albany, OR

- Beckley, WV Beckley, WV

- Bloomsburg-Berwick, PA

- California-Lexington Park, MD

- Carbondale-Marion, IL

- Chambersburg-Waynesboro, PA

- East Stroudsburg, PA

- Gettysburg, PA

- Grand Island, NE

- Grants Pass, OR

- Hammond, LA

- Hilton Head Island-Bluffton-Beaufort, SC

- Homosassa Springs, FL

- Kahului-Wailuku-Lahaina, HI

- Midland, MI

- New Bern, NC

- Sebring, FL

- Sierra Vista-Douglas, AZ

- Staunton-Waynesboro, VA

- The Villages, FL

- Walla Walla, WA

- Watertown-Fort Drum, NY

- Weirton-Steubenville, WV-OH