S&P Global and MSCI are making some major changes in the GICS sectors which will be enacted at the end of September. Under the old GICS, Telecommunications was one of the 11 GICS sectors which included primarily telephone companies. S&P Global and MSCI are changing the Telecommunications Sector to the Communications sector which includes not only Telecommunication Services, but Media and Entertainment stocks, which includes Advertising, Broadcasting, Cable & Satellite, Publishing, Movies and Entertainment, Interactive Home Entertainment and Interactive Media Services.

The most significant impact of these changes is that two companies that formerly were part of the Information Technology sector, Alphabet and Facebook, will be moved over to the Communications sector while Amazon has become part of the Consumer Discretionary sector since it is classified in the Internet & Direct Marketing Retail sub-industry. Although this leaves Apple and Microsoft in the Information Technology sector, this change has dramatically reduced the size of the Information Technology sector in the GICS. At the end of August 2018, the Information Technology sector represented 26% of the market cap of the S&P 500 while Telecommunications represented only 2%. These changes have turned the conservative, high-yielding Telecommunications sector into the high growth, low-yielding Communications sector. This reorganization of the GICS sector will balance out the two sectors by market cap more evenly.

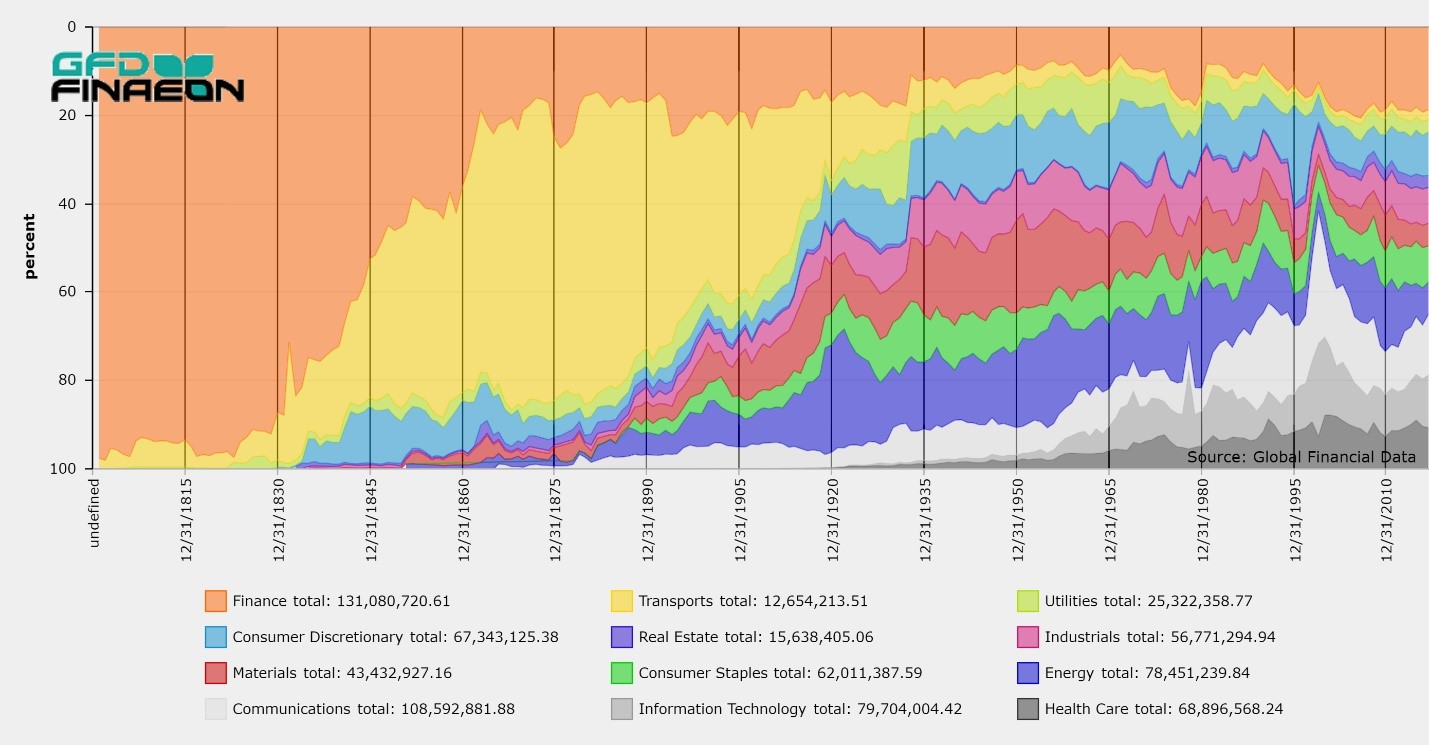

This raises the questions, however, as to how the Media & Entertainment market cap of the new Communications sector has grown over time. Global Financial Data has data on the American stock market going back to 1791 and has classified all of the stocks traded on American exchanges over the past 225 years by GICS and sector. We have been able to calculate how the Media & Entertainment stocks have grown within the Communications sector over the past 150 years. The graph below illustrates these changes.

S&P Global and MSCI are making some major changes in the GICS sectors which will be enacted at the end of September. Under the old GICS, Telecommunications was one of the 11 GICS sectors which included primarily telephone companies. S&P Global and MSCI are changing the Telecommunications Sector to the Communications sector which includes not only Telecommunication Services, but Media and Entertainment stocks, which includes Advertising, Broadcasting, Cable & Satellite, Publishing, Movies and Entertainment, Interactive Home Entertainment and Interactive Media Services.

The most significant impact of these changes is that two companies that formerly were part of the Information Technology sector, Alphabet and Facebook, will be moved over to the Communications sector while Amazon has become part of the Consumer Discretionary sector since it is classified in the Internet & Direct Marketing Retail sub-industry. Although this leaves Apple and Microsoft in the Information Technology sector, this change has dramatically reduced the size of the Information Technology sector in the GICS. At the end of August 2018, the Information Technology sector represented 26% of the market cap of the S&P 500 while Telecommunications represented only 2%. These changes have turned the conservative, high-yielding Telecommunications sector into the high growth, low-yielding Communications sector. This reorganization of the GICS sector will balance out the two sectors by market cap more evenly.

This raises the questions, however, as to how the Media & Entertainment market cap of the new Communications sector has grown over time. Global Financial Data has data on the American stock market going back to 1791 and has classified all of the stocks traded on American exchanges over the past 225 years by GICS and sector. We have been able to calculate how the Media & Entertainment stocks have grown within the Communications sector over the past 150 years. The graph below illustrates these changes.

With Jack Ma predicting that the trade wars between the United States and China could go on for another 20 years, Global Financial Data has added data on tariffs so our customers can analyze tariffs between countries and over time. With Donald Trump using tariffs as his primary weapon in his global trade wars, it is important to understand what tariff rates are throughout the world.

GFD has collected data from the World Bank covering over 2800 series on tariffs from every country in the world. The data include tariff rates for primary products, manufactured products and all products. It includes data on both the average tariff rates for countries as well as the most favored nation rates. The data begins in 1988 and extends up to 2016.

GFD has also collected data on U.S. tariffs going back to 1790 as the chart below shows.

With Jack Ma predicting that the trade wars between the United States and China could go on for another 20 years, Global Financial Data has added data on tariffs so our customers can analyze tariffs between countries and over time. With Donald Trump using tariffs as his primary weapon in his global trade wars, it is important to understand what tariff rates are throughout the world.

GFD has collected data from the World Bank covering over 2800 series on tariffs from every country in the world. The data include tariff rates for primary products, manufactured products and all products. It includes data on both the average tariff rates for countries as well as the most favored nation rates. The data begins in 1988 and extends up to 2016.

GFD has also collected data on U.S. tariffs going back to 1790 as the chart below shows.

The Vereenigde Oost-Indische Compagnie (VOC), or the United East India Company, was not only the first multinational corporation to exist, but also probably the largest corporation in size in history. The company existed for almost 200 years, from its founding in 1602, when the States-General of the Netherlands granted it a 21-year monopoly over Dutch operations in Asia, until its demise in 1796. During those two centuries, the VOC sent almost a million people to Asia, more than the rest of Europe combined. It commanded almost 5,000 ships and enjoyed huge profits from its spice trade. The VOC was larger than some countries. In part, because of the VOC, Amsterdam remained the financial center of capitalism for two centuries. Not only did the VOC transform the world, but it transformed financial markets as well.

The Vereenigde Oost-Indische Compagnie (VOC), or the United East India Company, was not only the first multinational corporation to exist, but also probably the largest corporation in size in history. The company existed for almost 200 years, from its founding in 1602, when the States-General of the Netherlands granted it a 21-year monopoly over Dutch operations in Asia, until its demise in 1796. During those two centuries, the VOC sent almost a million people to Asia, more than the rest of Europe combined. It commanded almost 5,000 ships and enjoyed huge profits from its spice trade. The VOC was larger than some countries. In part, because of the VOC, Amsterdam remained the financial center of capitalism for two centuries. Not only did the VOC transform the world, but it transformed financial markets as well.

The United East India Company Takes Over Asian Trade

The foundations of the VOC were laid when the Dutch began to challenge the Portuguese monopoly in East Asia in the 1590s. These ventures were quite successful. Some ships returned a 400 percent profit, and investors wanted more. Before the establishment of the VOC in 1602, individual ships were funded by merchants as limited partnerships that ceased to exist when the ships returned. Merchants would invest in several ships at a time so that if one failed to return, they weren’t wiped out. The establishment of the VOC allowed hundreds of ships to be funded simultaneously by hundreds of investors to minimize risk. The English founded the East India Company in 1600, and the Dutch followed in 1602 by founding the Vereenigde Oost-Indische Compagnie. The charter of the new company empowered it to build forts, maintain armies, and conclude treaties with Asian rulers. The VOC was the original military-industrial complex. The VOC quickly spread throughout Asia. Not only did the VOC establish itself in Jakarta and the rest of the Dutch East Indies (now Indonesia), but it established itself in Japan, being the only foreign company allowed to trade in Japan. The company traded along the Malabar Coast in India, removing the Portuguese, traded in Sri Lanka, at the Cape of Good Hope in South Africa, and throughout Asia. The company was highly successful until the 1670s when the VOC lost its post in Taiwan and faced more competition from the English and other colonial powers. Profits continued, but the VOC had to switch to traded goods with lower margins. They were able to do this because interest rates had fallen during the 1600s.

The chart below shows how the VOC’s revenue increased over time. Revenues were around 7.5 Million Guilders between 1650 and 1680 (about $3 million), increased to around 20 million Guilders (about $8 million) around 1720 and stayed at that level until 1780.

Lower interest rates enabled the VOC to finance more trade through debt. The company paid high dividends, sometimes funded through borrowing, which reduced the amount of capital that was reinvested. Given the high level of overhead it took to maintain the VOC outposts throughout Asia, the borrowing and lack of capital ultimately undermined the VOC and led to its demise. Nevertheless, until the 1780s, the VOC remained a huge multinational corporation that stretched throughout Asia.

The Fourth Anglo-Dutch War of 1780–1784 left the company a financial wreck. The French Revolution began in 1789, leading to the occupation of Amsterdam in 1795. The VOC was nationalized on March 1, 1796, by the new Batavian Republic, and its charter was allowed to expire on December 31, 1799. Most of the VOC’s Asian possessions were ceded to the British after the Napoleonic Wars, and the English East India Company took over the VOC’s infrastructure.

The VOC Provides Innovations in Finance

The VOC transformed financial capitalism forever in ways few people understand. Although shares had been issued in corporations before the VOC was founded, the VOC introduced limited liability for its shareholders, which enabled the firm to fund large-scale operations. Limited liability was needed since the collapse of the company would have destroyed even the largest investor in the company, much less small investors. Although this innovation changed capitalism forever, there were ways in which the VOC failed to transform itself, which led to its downfall. The company’s capital remained virtually the same during its 200-year existence, staying around 6.4 million florins (about $2.3 million). Instead of issuing new shares to raise additional capital, the company relied on reinvested capital. The VOC’s dividend policy left little capital for reinvestment, so the company turned to debt. The company first issued debt in the 1630s, increasing its debt/equity ratio to two. The ratio stayed at two until the 1730s, rising to around four in the 1760s, then increased dramatically in the 1780s to around eighteen, ultimately bankrupting the company, and leading to its nationalization and demise.

Dutch East India Stock Dividend Yield, 1650 to 1795

As the chart below shows, shares started at 100 in 1602, moved up to 200 by 1607, suffered a bear raid in 1609, moved up to the 400 range in the 1630s, fluctuated as the fortune of the company changed from year to year, participated in the bubble of the 1720s when shares exceeded 1,000, fell back to 600, rallied to 800 in the 1730s, then slowly declined from there. Perhaps no better indicator of the Dutch economy, or the global economy, prior to 1800 exists.

The Impact on the Amsterdam Stock Exchange

The VOC also transformed the Amsterdam Stock Exchange, causing a number of innovations to be introduced, such as futures contracts, options, short selling, and even the first bear raid. Isaac le Maire was the largest shareholder of the VOC in its early years, and he initiated the first bear raid in stock history, selling shares of VOC short in order to buy them back at a profit. These actions also led to the first government regulation of stock markets, attempting to ban short selling in 1621, 1623, 1624, 1630, and 1632, as well as banning options and other forms of financial wizardry. The fact that these laws had to be passed so many times shows that these regulations were not that effective. One problem for the long-term success of the Amsterdam Stock Exchange was that the VOC and the West Indies Company (WIC) were the only shares of importance that traded on the Amsterdam Stock Exchange. Between 1600 and 1800, no new large companies listed in Amsterdam. Although Dutch fiscal rectitude kept debt and interest rates low, it also helped stifle the growth of the Amsterdam Stock Exchange because government bonds never became a prominent part of the trading on the exchange. Due to the decentralized political nature of the Netherlands, government debt was held locally. There was no large centralized national debt as in France and England, and ultimately, this inhibited the growth of the Amsterdam Stock Exchange. The Netherlands was as decentralized as France was centralized. Because the VOC and WIC so dominated the share market, the company didn’t issue new shares to raise capital. Dutch debt was so small and diversified among its cities that the Dutch invested in foreign debt to find an outlet for their capital. Dutch newspapers of the 1700s often listed the prices of French debt in Paris as well as British Consols, Bank of England stock, the British East India Company and South Sea Company stock in London, but no other debt or equity from Amsterdam was listed. With the exception of colonial trade, until the 1800s no capitalist enterprise required the levels of capital of the VOC and WIC. So the Dutch capital that was available went into debt, not equity. America went to Amsterdam to raise capital, as did Sweden, France, England, Russia, Saxony, Denmark, Austria, and other countries. This provided Dutch investors with higher returns, but didn’t develop the Dutch economy in the way it could have. Unfortunately, the profitability of the Dutch East India Company was highly erratic as the chart below shows (there were 2.5 Guilder to 1 U.S. Dollar). Although there were many years when the VOC was profitable, there were also numerous years when the company lost money, and yet it still paid a dividend in most years, draining the capital of the company and forcing the VOC to take on more and more debt. The death knell of the company came in the 1770s and 1780s when the Fourth Anglo-Dutch War of 1780-1784 devastated the company’s finance. The company never recovered and it suffered losses for the rest of its life. The Netherlands were conquered by the French during the Napoleonic Wars and the company’s assets were seized by the British. The VOC ceased to exist in 1796.

The Financial Capital of the World Shifts to London

Before the Industrial Revolution, companies were simply too small to require sufficient capital to be traded on exchanges. Shipping had long been a high-risk venture, providing high returns and high losses, and investors diversified their risk by putting their money in a number of different ships. The colonial trading companies of the 1600s and 1700s took financial capital to a different level, allowing thousands of people to invest in hundreds of shipping ventures, diversifying their risk. After the Napoleonic Wars, the center of global finance shifted from Amsterdam to London. Although this process was spread out over several decades, it is amazing that the center of global finance could move from Amsterdam to London so quickly and so easily. There were some things, mostly political, which Amsterdam had little control over, such as the Napoleonic Wars, their occupation by the French, and the loss of its colonies after the war. In retrospect, there were things the Dutch could have done to keep Amsterdam at the center of global finance after 1815, but the trend was inevitable. The Dutch failed to diversify away from VOC and WIC shares and allow other companies to take advantage of local capital markets; they failed to sufficiently develop the bond side of the market because there was no centralized government debt until the late 1700s; they failed to expand the capital of the VOC, but instead chose to borrow, adding to the debt load, which led to the bankruptcy of the VOC and WIC; the VOC and WIC did not sufficiently reinvest dividends for growth; and they failed to offer a large number of securities that encouraged trading as in London. The company failed to raise additional capital when necessary, to limit borrowing, or to fund capital expenditures by cutting its dividend. Since the Netherlands lacked a centralized debt issuer, as the French, British, and Russians did, the Amsterdam Stock Exchange faded in importance after the VOC and WIC collapsed. Foreign government bonds became more prominent in Amsterdam, but even the foreign government bond trading moved to London in the 1820s, where capital was more readily available. It is doubtful whether Amsterdam could have foreseen all the changes that happened, and perhaps they couldn’t have prevented the move of the world’s financial capital from Amsterdam to London that occurred after 1815, but it was a lesson London should have learned. London became the engine of global capitalism for the 19th century, only to lose its place to New York after World War I. The US should understand this lesson as well. The global center of finance must grow, innovate, and be as open as possible. Otherwise, the center will move to someplace that is. Because of the breadth of data that Global Financial Data provides in its UK and US Stock Database, providing data from 1601 to 2018, GFD runs into problems of coverage that no other database encounters. Today, stocks trade thousands or even millions of shares on a daily basis. Data on stock prices, shares outstanding and corporate actions are kept in exacting detail by the exchanges and by data providers and calculating indices poses few problems because computers can use their algorithms to spin out thousands of results on a daily basis. Unfortunately, this was not always the case.

In the 1800s, stock volume was often extremely low and many stocks did not trade over the course of an entire month. The low volume day for the New York Stock Exchange was March 16, 1830 when only 31 shares traded on the entire exchange. Up until the 1870s, the New York Times was able to list every trade on the NYSE in each issue as did the London Times for stocks traded in London. Today thousands of shares trade every nanosecond.

To calculate price and return indices, you need three things, price data, corporate actions and shares outstanding. Global Financial Data has done everything it can to obtain as complete a record of prices, corporate actions and shares outstanding as is possible, but the further back you go in time, the more difficult it is to obtain this information.

Because of the breadth of data that Global Financial Data provides in its UK and US Stock Database, providing data from 1601 to 2018, GFD runs into problems of coverage that no other database encounters. Today, stocks trade thousands or even millions of shares on a daily basis. Data on stock prices, shares outstanding and corporate actions are kept in exacting detail by the exchanges and by data providers and calculating indices poses few problems because computers can use their algorithms to spin out thousands of results on a daily basis. Unfortunately, this was not always the case.

In the 1800s, stock volume was often extremely low and many stocks did not trade over the course of an entire month. The low volume day for the New York Stock Exchange was March 16, 1830 when only 31 shares traded on the entire exchange. Up until the 1870s, the New York Times was able to list every trade on the NYSE in each issue as did the London Times for stocks traded in London. Today thousands of shares trade every nanosecond.

To calculate price and return indices, you need three things, price data, corporate actions and shares outstanding. Global Financial Data has done everything it can to obtain as complete a record of prices, corporate actions and shares outstanding as is possible, but the further back you go in time, the more difficult it is to obtain this information.